10.04.2026

News

Monthly Recap: March 2026

As the first quarter draws to a close, we take the opportunity to review the performance of our strategies and share a brief perspective on the current market environment.

March was characterized by elevated volatility, largely driven by ongoing geopolitical tensions in the Middle East. Against this backdrop, our strategies delivered the following results:

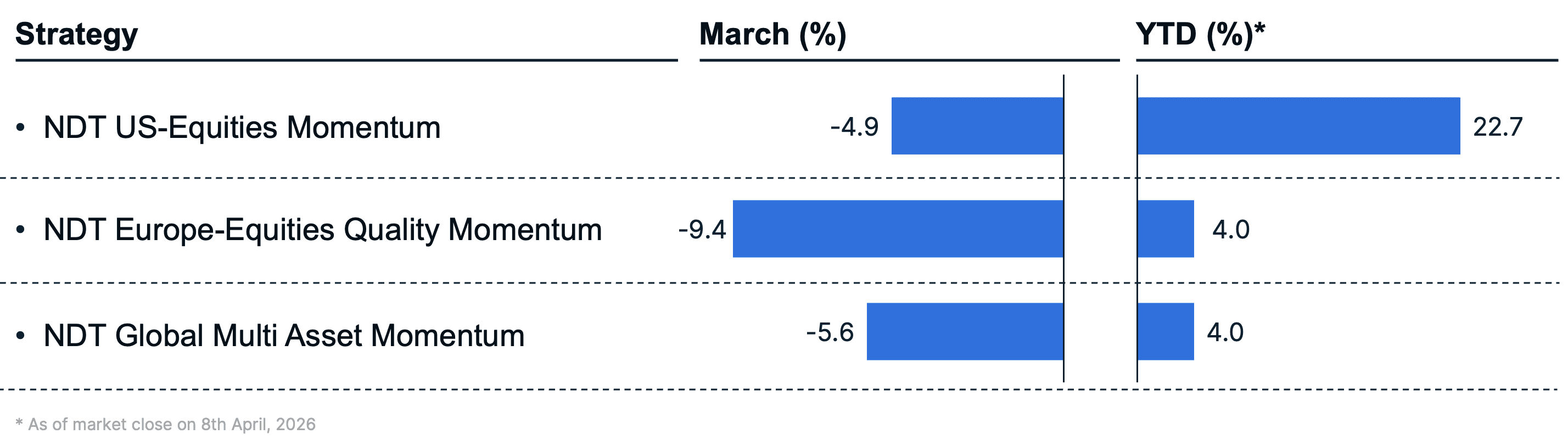

The NDT US Equities Momentum strategy returned -4.9% (benchmark: -3.0%), the NDT Europe Equities Quality Momentum strategy -9.4% (benchmark: -7.7%), and the NDT Global Multi Asset Momentum model -5.6% (benchmark: -5.1%).

Q1 Performance Update (as of the close of April 8, 2026)

NDT US-Equities Momentum strategy is up +22.7%, significantly ahead of its benchmark which sits at -0.7%.

NDT Europe-Equities Quality Momentum strategy delivered +4.0% versus +4.4% for its benchmark

NDT Global Multi Asset Momentum strategy gained +4.0% compared to +1.4% for the benchmark.

We are encouraged by how our rule-based, data-driven approach has navigated a challenging and rapidly shifting market environment in the last couple of months. The results underline our core belief: "Momentum does not predict the future, it identifies where capital is flowing."

Looking ahead, a potential easing of geopolitical tensions could act as a catalyst for a relief rally. In this context, we continue to see the current environment as an attractive entry point for both new and additional allocations.

Last Month's Strategy Returns

Market Commentary

US Equities & Economic Backdrop: US stocks fell sharply in March as a major escalation in the US-Iran conflict shifted the market's focus from solid fundamentals to geopolitical risk. Broad US benchmarks dropped between 4.5% and 6%, with the S&P 500 Equal Weight Index down 6%, even though earnings remain healthy and S&P 500 Q1 EPS is still expected to grow about 13% year-on-year, the sixth straight quarter of double-digit growth.

Key Drivers: The selloff was driven by macro de-risking rather than a style rotation, with both growth and value declining together across large and small caps. Energy supply disruptions in the Middle East drove one of the largest oil shocks in decades, reigniting inflation worries and reducing the Fed's room to cut rates if growth slows.

Eurozone & Global: European equities were mixed: the MSCI Europe ex-UK fell 2.3% on geopolitical tensions, while the UK's FTSE All-Share gained 2.4%, helped by its commodity exposure. Japan's TOPIX rose 3.6%, supported by a weaker yen and a ruling-party election win, while emerging markets were broadly flat with Asia ex-Japan down 1.1%.

Rates, Sectors & Themes: Treasury yields jumped, with the 2-year up 42bps to 3.79% and the 10-year up 38bps to 4.32% as investors pared back rate-cut expectations. Energy was the only positive S&P 500 sector, while every other large-cap sector finished lower, including both cyclicals like Industrials and defensives like Healthcare and Staples.

Commodities & Other Assets: Commodities were the standout, with the Bloomberg Commodity Index posting its strongest month since May 2009. Brent crude surged 63%, its biggest monthly jump since the 1970s, but traditional inflation hedges failed to play their usual role: gold fell 11.6% and silver dropped 19.9% as real yields rose and the US dollar strengthened.

Our Top and Worst Performers in the US

Below are the two top and worst performers from our NDT US-Equities Momentum Strategy in March:

Ciena Corp | +9.7% | Networking

AI-driven optical networking demand fueled the rally. Q1 revenue came in at $1.52B, up 24% year-over-year, and adjusted EPS hit $0.88, beating consensus of $0.72, with gross margins expanding to 46.2%.

Sandisk Corp | +2.5% | Memory & Storage

NAND prices kept climbing as the structural shortage tightened. Contract prices surged nearly 38% in Q1 2026, and hyperscaler demand more than offset other losses, helping the stock extend a rally that pushed YTD gains to well over 150%.

Main Drags during March:

Micron Technology Inc | -15.9% | Semiconductors

Despite Q2 revenue of $23.86B and ~80% margin guidance, shares fell over 30% in eight sessions, before recovering partially, as investors took profits. Citi flagged peak-margin worries and a Google breakthrough raised fears of weaker memory demand.

Lockheed Martin Corp | -11.6% | Defense

Shares slid as investors took profits after a strong run in 2026. Even new production wins like the Pentagon agreement to quadruple Precision Strike Missile output failed to lift the stock, with competing defense headlines limiting upside.

Our Top and Worst Performers in Europe

Below are the two top and worst performers from our NDT Europe-Equities Quality Momentum Strategy from March:

Nordex SE | +7.0% | Wind & Renewables

The wind turbine maker climbed on a steady stream of new orders. In late March it secured a significant new order for a project in Serbia, lifting its total portfolio and including a 30-year Premium Service contract.

Bunzl PLC | +6.1% | Distribution

Shares ended March higher despite a soft FY25 update: revenue rose 3.0% at constant FX to £11.85B, but adjusted operating profit fell slightly to £910.3M and the operating margin contracted to 7.7% from 8.3% in the prior year.

Main Drags during March:

Indra Sistemas SA | -24.9% | Defense & IT

Shares pulled back heavily even after Indra was added to the FTSE All-World Index and rolled out an AI-powered apron monitoring system across Spain's three busiest airports, as investors flagged execution strain from rapid hiring and expansion, though the stock recovered partially in April.

Unilever PLC | -22.8% | Consumer Staples

Shares declined during the month after Unilever announced a definitive agreement to merge its global Foods division with McCormick in a $44.8B transaction structured as a tax-efficient spin-off and merger, leaving a more focused group centered on Beauty and Personal Care.

NDT US-Equities Momentum:

A satellite solution to complement existing portfolios with a concentrated selection of US large-cap stocks with strong momentum.

NDT Europe-Equities Quality Momentum:

Complement your portfolio with a selection of high-momentum and quality stocks out of the STOXX Europe 600.

NDT Global Multi Asset Momentum:

A systematic strategy designed to complement discretionary portfolios for long-term participation in global growth.

As we move further into the year, we continue to monitor developments closely and expect conditions to gradually stabilize. At the same time, we remain focused on navigating the environment with our disciplined, systematic approach.

If you have any questions or would like to connect, we look forward to hearing from you.

Best regards,

Adrian, Andreu & Loris

For marketing purposes only. Advertising according to Art. 68 FinSA. All rights reserved.

Photo by İrfan Simsar

As the first quarter draws to a close, we take the opportunity to review the performance of our strategies and share a brief perspective on the current market environment.

March was characterized by elevated volatility, largely driven by ongoing geopolitical tensions in the Middle East. Against this backdrop, our strategies delivered the following results:

The NDT US Equities Momentum strategy returned -4.9% (benchmark: -3.0%), the NDT Europe Equities Quality Momentum strategy -9.4% (benchmark: -7.7%), and the NDT Global Multi Asset Momentum model -5.6% (benchmark: -5.1%).

Q1 Performance Update (as of the close of April 8, 2026)

NDT US-Equities Momentum strategy is up +22.7%, significantly ahead of its benchmark which sits at -0.7%.

NDT Europe-Equities Quality Momentum strategy delivered +4.0% versus +4.4% for its benchmark

NDT Global Multi Asset Momentum strategy gained +4.0% compared to +1.4% for the benchmark.

We are encouraged by how our rule-based, data-driven approach has navigated a challenging and rapidly shifting market environment in the last couple of months. The results underline our core belief: "Momentum does not predict the future, it identifies where capital is flowing."

Looking ahead, a potential easing of geopolitical tensions could act as a catalyst for a relief rally. In this context, we continue to see the current environment as an attractive entry point for both new and additional allocations.

Last Month's Strategy Returns

Market Commentary

US Equities & Economic Backdrop: US stocks fell sharply in March as a major escalation in the US-Iran conflict shifted the market's focus from solid fundamentals to geopolitical risk. Broad US benchmarks dropped between 4.5% and 6%, with the S&P 500 Equal Weight Index down 6%, even though earnings remain healthy and S&P 500 Q1 EPS is still expected to grow about 13% year-on-year, the sixth straight quarter of double-digit growth.

Key Drivers: The selloff was driven by macro de-risking rather than a style rotation, with both growth and value declining together across large and small caps. Energy supply disruptions in the Middle East drove one of the largest oil shocks in decades, reigniting inflation worries and reducing the Fed's room to cut rates if growth slows.

Eurozone & Global: European equities were mixed: the MSCI Europe ex-UK fell 2.3% on geopolitical tensions, while the UK's FTSE All-Share gained 2.4%, helped by its commodity exposure. Japan's TOPIX rose 3.6%, supported by a weaker yen and a ruling-party election win, while emerging markets were broadly flat with Asia ex-Japan down 1.1%.

Rates, Sectors & Themes: Treasury yields jumped, with the 2-year up 42bps to 3.79% and the 10-year up 38bps to 4.32% as investors pared back rate-cut expectations. Energy was the only positive S&P 500 sector, while every other large-cap sector finished lower, including both cyclicals like Industrials and defensives like Healthcare and Staples.

Commodities & Other Assets: Commodities were the standout, with the Bloomberg Commodity Index posting its strongest month since May 2009. Brent crude surged 63%, its biggest monthly jump since the 1970s, but traditional inflation hedges failed to play their usual role: gold fell 11.6% and silver dropped 19.9% as real yields rose and the US dollar strengthened.

Our Top and Worst Performers in the US

Below are the two top and worst performers from our NDT US-Equities Momentum Strategy in March:

Ciena Corp | +9.7% | Networking

AI-driven optical networking demand fueled the rally. Q1 revenue came in at $1.52B, up 24% year-over-year, and adjusted EPS hit $0.88, beating consensus of $0.72, with gross margins expanding to 46.2%.

Sandisk Corp | +2.5% | Memory & Storage

NAND prices kept climbing as the structural shortage tightened. Contract prices surged nearly 38% in Q1 2026, and hyperscaler demand more than offset other losses, helping the stock extend a rally that pushed YTD gains to well over 150%.

Main Drags during March:

Micron Technology Inc | -15.9% | Semiconductors

Despite Q2 revenue of $23.86B and ~80% margin guidance, shares fell over 30% in eight sessions, before recovering partially, as investors took profits. Citi flagged peak-margin worries and a Google breakthrough raised fears of weaker memory demand.

Lockheed Martin Corp | -11.6% | Defense

Shares slid as investors took profits after a strong run in 2026. Even new production wins like the Pentagon agreement to quadruple Precision Strike Missile output failed to lift the stock, with competing defense headlines limiting upside.

Our Top and Worst Performers in Europe

Below are the two top and worst performers from our NDT Europe-Equities Quality Momentum Strategy from March:

Nordex SE | +7.0% | Wind & Renewables

The wind turbine maker climbed on a steady stream of new orders. In late March it secured a significant new order for a project in Serbia, lifting its total portfolio and including a 30-year Premium Service contract.

Bunzl PLC | +6.1% | Distribution

Shares ended March higher despite a soft FY25 update: revenue rose 3.0% at constant FX to £11.85B, but adjusted operating profit fell slightly to £910.3M and the operating margin contracted to 7.7% from 8.3% in the prior year.

Main Drags during March:

Indra Sistemas SA | -24.9% | Defense & IT

Shares pulled back heavily even after Indra was added to the FTSE All-World Index and rolled out an AI-powered apron monitoring system across Spain's three busiest airports, as investors flagged execution strain from rapid hiring and expansion, though the stock recovered partially in April.

Unilever PLC | -22.8% | Consumer Staples

Shares declined during the month after Unilever announced a definitive agreement to merge its global Foods division with McCormick in a $44.8B transaction structured as a tax-efficient spin-off and merger, leaving a more focused group centered on Beauty and Personal Care.

NDT US-Equities Momentum:

A satellite solution to complement existing portfolios with a concentrated selection of US large-cap stocks with strong momentum.

NDT Europe-Equities Quality Momentum:

Complement your portfolio with a selection of high-momentum and quality stocks out of the STOXX Europe 600.

NDT Global Multi Asset Momentum:

A systematic strategy designed to complement discretionary portfolios for long-term participation in global growth.

As we move further into the year, we continue to monitor developments closely and expect conditions to gradually stabilize. At the same time, we remain focused on navigating the environment with our disciplined, systematic approach.

If you have any questions or would like to connect, we look forward to hearing from you.

Best regards,

Adrian, Andreu & Loris

For marketing purposes only. Advertising according to Art. 68 FinSA. All rights reserved.

Photo by İrfan Simsar